For most individuals managing an SMSF well is difficult – it requires time, effort and investment expertise. The emergence of robo-advice in Australia over the last four years and popularity of ETFs has generated an increase in SMSF trustees allocating part of their fund to a robo-advice service to manage.

This is in part because robo advice is the fastest growing area of wealth management globally, expected to grow to US$2.2 trillion or 5% of all money managed by 2020. Considering that SMSFs are the largest segment of the Australian superannuation industry, managing $653.8 billion as at December 2016, it’s inevitable more SMSFs will turn their attention towards robo-advice. In Australia this trend is in its infancy however 2017 is shaping up to be the year more SMSFs start using robo advice.

Robo-advice… what’s in it for SMSFs?

SMSFs offer more control over your super. However, many people come to realise that managing an SMSF is a full-time job. It’s time consuming, requires specific investment expertise and discipline to effectively manage your own money.

A US investment research firm found that over a period of more than 20 years the average self-managed investor loses approximately 4% per year due to behavioural mistakes.[1]

Robo-advisers automate many processes that are prone to emotion and therefore mistakes. This includes choosing the right products, portfolio asset allocation, rebalancing and reinvestment. Automating these processes saves time, costs and removes many of the investment temptations that are likely to harm returns.

For example, when an investment portfolio significantly moves away from its target asset allocation a robo-adviser rebalances so it does not become riskier over time. As an individual DIYing these decisions can be complex and a time vacuum.

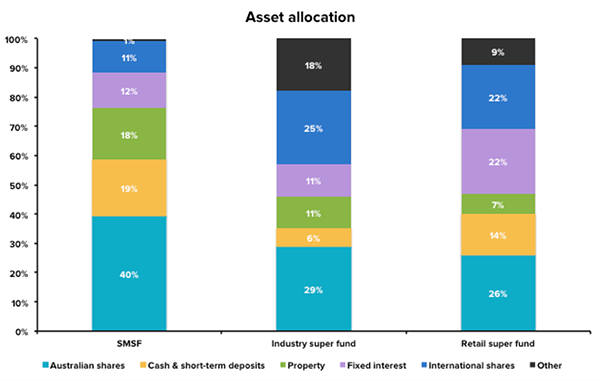

It’s not only bad behaviour and lack of time… The highest risk for poor performance in an SMSF is portfolio allocation and over exposure to certain assets such as Australian shares, cash and term deposits and property.

Source: Multiport, APRA Annual Superannuation Bulletin 2014.

Sadly, ATO figures show 44 percent of SMSFs have not made a return over the past seven years. This is worrying but not surprising as SMSF investors are not immune to the behavioural biases that plague most self-directed investors – over trading, chasing hot markets and panicking when the market falls! All of these are emotional actions that harm long-term returns.

The problem with these types of portfolio is the lack of diversification and over exposure to home country risks (ie the Australian economy) and SMSFs miss out on returns from investments like global shares. We’ve written extensively about SMSF portfolio risks here.

Robo-advice = smarter diversification

To address the typical concentration risk within a SMSF Stockspot’s portfolios use ETFs that are made up of investments in over 1,400 shares and bonds from Australia and around the world.

Our portfolios have between 65% and 75% of their holdings in Australian shares and bonds. This helps limit the impact of short-term currency movements on overall portfolio value.

Overseas investments are also important to reduce the reliance on Australian companies; 15-25% of our portfolios are allocated towards international investments. The highest international allocation is the US at 4.7% to 9.2% of the portfolios, followed by Asia (ex China), Europe and then China.

Between 2010 and 2016, most global share markets performed better than Australian shares. Even when Australian shares start to perform well again, an international allocation helps reduce the overall risk.

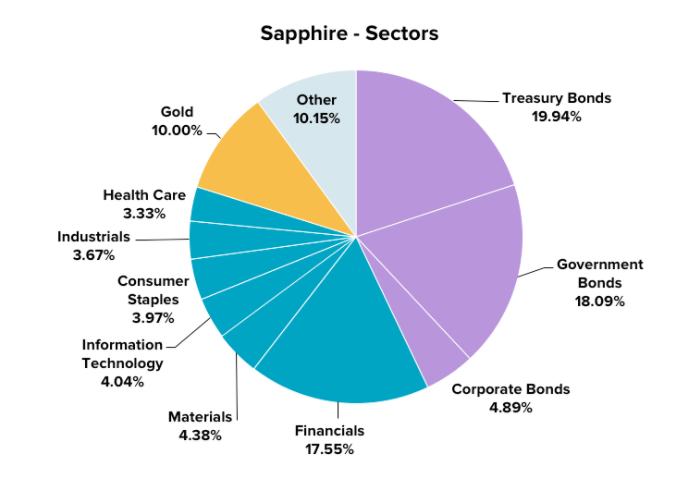

Including global shares means healthcare and IT sectors feature more than they would in most SMSF portfolios. Meanwhile fixed interest is the largest components of the more conservative Sapphire and Amethyst portfolios to reduce volatility and draw-down risk closer to retirement.

Here’s an example of our moderately conservative portfolio: sapphire.

Our allocation to gold across all portfolio strategies helps reduce risk and steady returns during times of market turmoil. Think of it like an insurance policy.

How SMSFs use Stockspot

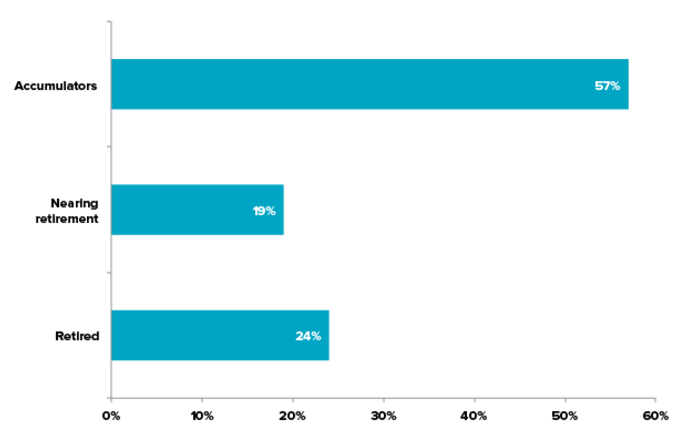

One our fastest growing client segments are SMSF investors. This is interesting because a lot of media coverage on digital investment services, has until recently, categorised it as investment for millennials.

When we look at the investment profile of our SMSF investors they fall into one of the following life stages:

The average fund size of a Stockspot SMSFs investor is about $800,000. This is below the average national balance of $1 million as most of our investors in the accumulator stage.

The majority of SMSF investors choose our Amethyst (conservative growth) portfolio

Interestingly over a quarter of SMSF investors choose our Turquoise (‘balanced growth’) portfolio, reflecting the accumulator demographic in their 40s still building their wealth.

The SMSF market will continue to expand and we believe robo-advice will play a central role in future SMSFs portfolios.

[1] http://www.qidllc.com/wp-content/uploads/2016/02/2016-Dalbar-QAIB-Report.pdf.

Lauren Franz | Stockspot

- Is your super trapped in a Fat Cat Fund? - 13 October 2017

- Stockspot – Partner Program for Accountants - 28 August 2017

- Stockspot Media Release: Stirling Mortlock joins Australia’s largest robo-adviser - 31 July 2017