The construction of financial statements does not have to be the onerous task that many people dread. By taking a ‘scientific’ approach and breaking it down into a series of steps, the process can be quite easily managed. Or at least that is the view of Michael Berrington and Vik Bhandari who between them boast more than 40 years of experience in the preparation of financial statements.

The following is an extract from their complimentary booklet entitled Construction of Financial Statements which is available for download by following this link:

http://content.ifrssystem.com/content/PFS/ConstructionOfFinancialStatements.pdf

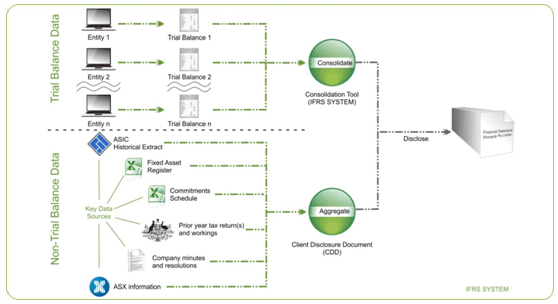

Gathering Source Documentation

The construction process begins with gathering all of the source documents that will be needed. Source documentation includes both financial and non-financial data as shown by the example in the following diagram:

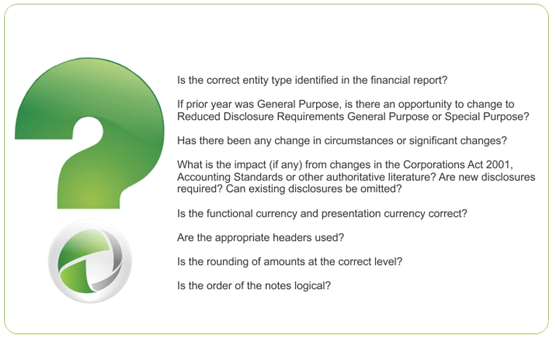

Preliminary Questions

Once all of the source information has been gathered, there are a number of preliminary questions (see booklet for details) that should be addressed.

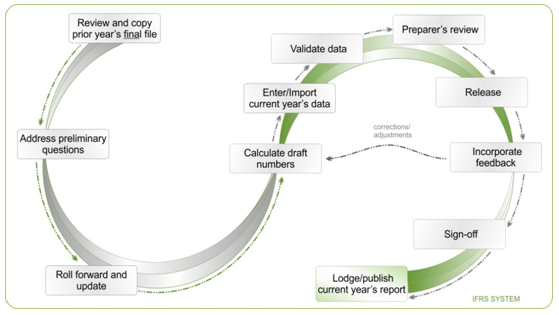

The Construction process

Completion of the following steps will result in a ‘first draft’ of the financial statements. The first draft will serve as the platform from which the ‘final’ financial statements will evolve.

- Retrieve and copy the prior year’s final version of the file.

- Apply all changes that result from the answers to the ‘preliminary questions’.

- Roll forward the numbers, headers general disclosure from current to comparatives.

- Update the template to ensure compliance with any new requirements/standards.

- Calculate the 1st draft of the statement of comprehensive income and statement of financial position (excluding tax).

- Calculate the 1st draft of the tax disclosures and incorporate these numbers into the statement of comprehensive income and statement of financial position.

- Calculate the 1st draft of business combinations (if applicable).

- Calculate the 1st draft of the statement of cash flows and related reconciliation note.

- Calculate the 1st draft of the financial instruments (if applicable).

- Calculate the 1st draft of the deed of cross guarantee (if applicable).

- Enter the current year disclosures, including financial and non-financial information.

- Disclose any significant changes.

- Check the disclosures back to the source information, to ensure that they agree.

- Perform an adds-check, cross-reference check and overall sense-check.

- Self-review the financial statements and correct any errors or omissions found based on the guidance provided in the booklet.

- Release the financial statements for review.

- What does 2021 have in store for ATO audit activity? - 26 November 2020

- Over 30,000 people have invested in crowd sourced funding equity raising - 13 August 2019

- The 7 things your SMSF clients are judging you on - 13 June 2019